CFI Newsletter #16: India's Carbon Sink

+ Limiting to 1.5°C warming; USD 1 trillion into solar; Climate tech funding boom in India; and everything COP26

The Climate Finance Initiative Newsletter offers quick digests and insights around what is happening in climate finance. While the Climate Finance Initiative’s current focus of work is India-centric, we will capture a global perspective of climate finance in this newsletter on a fortnightly basis.

We write this newsletter as COP26 is about to start in Glasgow. From India refusing to make a net zero commitment to Australia staunchly holding on to coal, the run-up to COP has been underwhelming at best. Which made us curious as to why this is being hailed as as crucial COP.

After all our research, all we can make out it that this is that psychological check point. COVID-19 put hold to a COP in 2020 so this is the meeting that is happening “5 years after Paris”. COP26 is therefore, being looked at as a chance to do a much needed stock taking and possibly course correct and set new targets for 2025.

We will be following the next week closely to see how the world leaders set the path for the next five years. In the meantime, we bring you top things on our mind as the biggest spotlight on climate action kicks off.

Climate Finance by the Numbers

5%

The probability that the world will be less than 1.5°C warmer, based on current emission reduction commitments by all nations

If you want a mark for why COP26 is likely to be an underwhelming summit, this little probability nugget from the International Energy Agency explains it. We stand only a 5% change of limiting global temperature increase to the 1.5°C mark where adverse climate effects can be expected to be limited. It is as good as unattainable. A 2.1°C warming limit has a 50% chance of being achieved with current policies, but that is reliant on all carbon mitigation commitments being achieved, which is not guaranteed at all.

There has been a set of lacklustre commitments from most countries. Ones that have net-zero pledges have scant to nothing detail on how they will get there. India has stated that they will not commit to a net-zero pledge until financing commitments are met. Which brings us to the USD 100 billion per year in climate finance that rich countries in 2009 promised to achieve by 2020 target that has been met entirely - the latest year for figures, 2019 did achieve USD 80 billion in financing to developing countries. This is not an insignificant figure, but reducing carbon emissions, limiting warming potential, and adapting to climate change, needs targets to be met, not good effort attempts that are nearly there.

From Copenhagen in 2009, the past 12 years - other than the brief positive of Paris in 2015 - has been a story of ineffective compromise, uncompromising stances, and finger-pointing, that really cannot be afforded for an issue that affects us all, but is perhaps the nature of trying to get 200+ countries to come together and align to a common path.

Unfortunately, the end result is that every day it does become more difficult to reach the targets we need to get to. But COP26 may throw some nice surprises.

$1 trillion

A planned USD 1 trillion dollar investment in solar energy is perhaps the sort of pick-me-up the COP26 summit.

The One Sun One World One Grid (OSOWOG) plan, led by India and the UK under the International Solar Alliance, is a global generation and distribution system that aims to provide solar energy to 140 countries.

Regional energy systems have been planned, such as the Australia-Singapore energy sharing project, and the functioning Nord Pool, which connects Scandinavian countries, but OSOWOG is the first one at a global scale.

OSOWOG matches generation based where the sun is shining, and demand, transporting it to where it is needed - it emphasizes direct consumption over energy storage. Solar energy will be sent across high-voltage direct cables across continents, even from under the ocean, to needy countries. The reduced need for energy storage systems can potentially can remove a significant cost barrier, but there are rumblings that electricity through deep-sea cables will negate the cost advantages of cheap solar.

India is seen as the centre of this network. After years of failing to meet the grid share and investment targets of solar energy in the country, this could be the tipping point that transforms the sector.

But as with all trillion dollar grandiose plan, there are also quite fundamental questions that need to get answered. For starters, building consensus between 140 countries with different roles to avoid a “Russia flexes its gas muscle to Europe during tense times”-like situations. There’s also the balancing act between needing to move fast, with the patience required to translate a grand vision to on-ground realities in 140 countries.

But OSOWOG has got a few things going for it.

The network incentivizes countries with high-generation potential to build more solar capacity as energy exports become a lot more accessible. Less-developed connected countries do not need to invest in solar plants immediately to start tapping into clean energy sources. And of course, there is the USD 1 trillion investment. Bloomberg Philanthropies has announced a partnership with the ISA to mobilise the amount, which is encouraging, but it is quite a while away to becoming a reality.

With a South Asia power pool being mooted as one of the first pilot projects in the near-term, the first of hopefully a lot more, OSOWOG is definitely worthy of a “Watch this space” tag.

$1 billion

Total venture capital funding received for climate tech in India between 2016-2021

Finance gets centre stage at all climate action discussions. India, in particular, has been extremely vocal about the need for developed nations to fund emission reduction since (in India’s view) they contributed to much of the emissions that have occurred so far.

Irrespective of who funds it, there is no denying that the world needs a lot of climate finance to reach the emission reduction goals we have set ourselves. A new Dealroom.co report shows that things are headed in the right direction there. 2021 is a record year for venture capital flowing into climate finance, with $32 billion raised this year so far. This is almost a 5x increase compared to 2016.

India lags behind US, China and Europe with total climate tech venture investments of $1 billion between 2016-2021 YTD. That, however, may not be the complete picture. We have seen several green shoots in climate finance in just the last year:

Renew Power, India’s largest renewable energy developer, listed on Nasdaq via a SPAC with a $4.5 billion valution;

A KKR backed InvIT raised INR 4.6 billion for investment in renewable energy;

Indian companies have raised more than $6 billion in green bonds in 2021 thus far, with Vector Green raising $166 million in the largest ever domestic green bond issuance.

Larry Fink remarked last week that the next 1000 unicorns (startups with >$1 billion valuation) will be in climate tech. With electric vehicle and agri-tech companies raising large rounds, we hope that at least a handful of these will be from India.

THE BIG READ

India’s Carbon Sink

In the run up to COP 26 in Glasgow, we dig into the 3rd and often less prominent of India’s climate change commitments to the Paris Agreements to understand how effective it is for tackling carbon emissions.

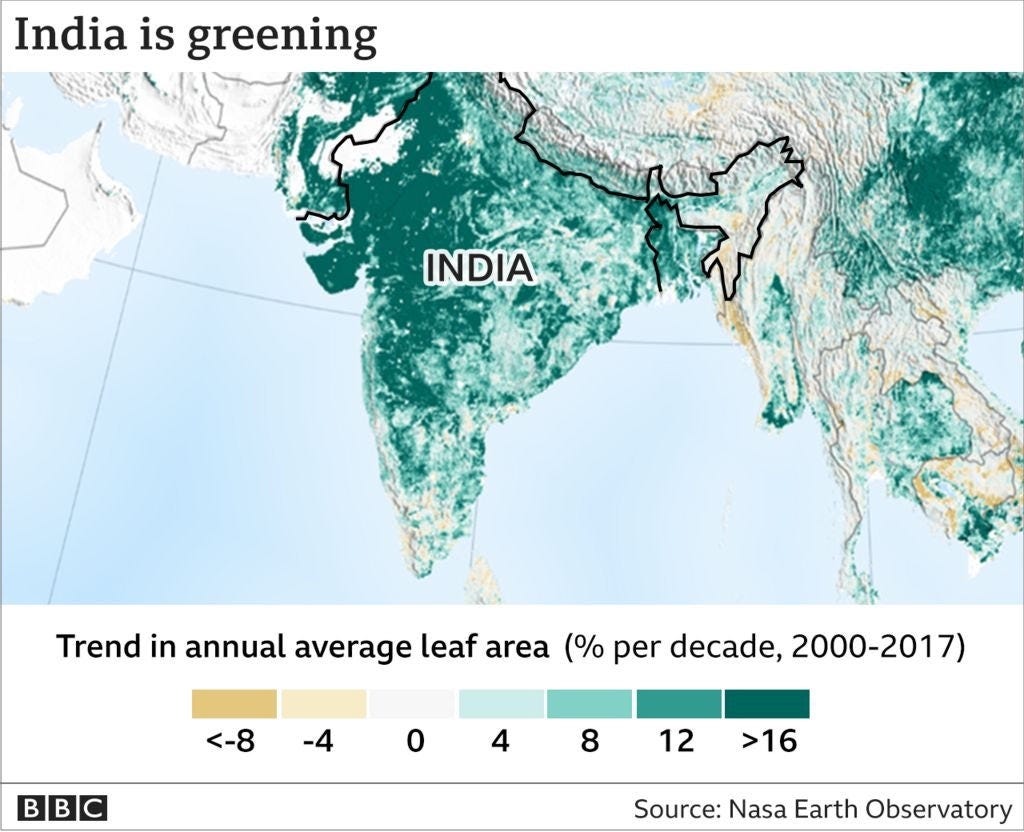

In 2019, a NASA study (a legitimate NASA study) found that there was 5.5 million square kilometres of extra green leaf area in the world in 2017 compared to 2000. Seven percent of this increase was in India, a surprising statistic when the general notion of emerging economies is an increase in land degradation, such as the cutting down of forest land, due to over-exploitation.

This news was taken as a mark of India's commitment to its 3rd Paris Agreement macro-target:

to create an additional (cumulative) carbon sink of 2.5–3 GtCO2e through additional forest and tree cover by 2030

But there is more to this.

For instance, 82% of that green cover growth in India was from cropland being added - due to increase in food demand and production - while only 4.4% was attributed to forests. Croplands and plantations taken in around 50% less carbon dioxide compared to forests land, on a per hectare basis.

It is worth taking a look at what is happening with forest-based carbon sequestration in India, on ground, and below ground.

What is India’s forest carbon stock?

Well, we are not entirely sure.

Here is a bit of a stats-heavy context setting.

Going by the government’s India State of Forests Report 2019 (ISFR 2019), the country’s carbon stock from forests (we include plantation land in this as well) in India in 2019 was estimated at 26.12 billion tonnes of CO2 equivalent (CO2-eq). This is from forest areas that are more than 1 hectare in size. Tree cover in areas less than 1 hectare adds an estimated 10 to 12% more of carbon sink space - around 3 billion tonnes, which brings our overall tree-related carbon sinks to around 29 billion tonnes of CO2-eq. Annoyingly but understandably this is not observed well in the ISFR - the gospel for such data.

Carbon stock is not the annual amount sequestered, but the overall store of carbon dioxide that forests can take in. For an idea of how much GHG is sequestered by forests and trees annually in India, in 2016, the number was around 300 million tonnes of CO2-eq.

The target to expand the carbon dioxide store through forest sequestration by 2.5-3Gt CO2-eq - from a baseline of 2015 - by 2030, means that every year, the area for carbon sequestration has to increase by between 165 to 200 MtCO2e.

This actual growth is either 71.8 million tonnes CO2eq, 128 million tonnes, or 35 million tonnes - all from government sources issued in 2019, mind you - but all significantly under the required annual increase in carbon stock to meet the Paris Agreement target. Deforestation rates as well, calculated by other sources, conflict a fair bit the growth numbers covered here (more on this later).

A 1500-word newsletter is not the place to parse through what the correct number is. What is clear though is that irrespective of where India is with its carbon stock today, the rate of growth needs to increase significantly.

So what is happening in India to increase its forest carbon stock?

It is quite a barren landscape

India’s current forest covers 24% of the country (although, of course, depending on your definition of forests you can come up with different numbers.) The government as part of its National Mission for a Green India has a target of achieving 33% of forest cover by 2030. It was first set in the 1952 Forest Policy when the focus was on improving biodiversity and tribal land areas, and where the idea of carbon stock was non-existent. But the 33% target does conveniently align with increasing it. A 9% increase in forest cover would undoubtedly lead to that 2.5-3 Gt CO2-eq target being met.

There are a raft of central and state government programs by different ministries and departments that converge on that tree cover target, through different core purposes.(For instance, the Ministry of Agriculture and Farmer’s Welfare’s Sub-Mission on Agro-forestry focuses on creating economic livelihood opportunities through forestry as a means to preserve them.) They cover a wide range:

improving or restoring natural forests and the tree density;

tree planting on wastelands, rural lands, roads and highways, and railway lines;

greening of urban spaces;

and agro-forestry.

The Ministry of Environment, Forests and Climate Change (MoEFCC) initiatives, arguably the most expansive, are off-pace and reflective of the overall need to do more - a Parliamentary Committee in 2018 found the MoEFCC’s initiatives to be “grossly under-funded”.

Reflective of this is the Green India Mission. With a 10 year target from 2015 to 2025 to increase forest and tree cover on 5 million hectares and improve the quality of forest cover on another 5 million hectares, it has only achieved 2.8% of its target as of 2021.

We cannot miss the soil for the trees

The role of soil as a carbon sink highlights why afforestation efforts to compensate for cutting down trees for development are not a like-for-like solution for carbon sequestration. Trees contain 32% of India’s forest-based carbon stock. 56% of India’s carbon stock is stored in the soil, most prominently the one which is in pristine environments not affected by deforestation.

The most sure fire way to preserve soil environments is not to cut down forestland for development. Afforestation projects to compensate for trees cut down miss out on the importance of soil as a carbon stock, notwithstanding lost biodiversity which requires a focus of its own.

Deforestation is not just a factor of forestland cut down for development. Natural causes such as forest fires have been increasing as weather conditions warm due to to climate change.

The 2019 IFSR found that even as tree cover was increasing, dense, pristine forests, especially in the North-East of the country were facing reductions in tree cover and carbon stock, and the store of carbon in the soil of forest land that has been deforested. The Global Forest Watch estimates that India’s lost 5% of its tree cover since 2000, equivalent to a carbon loss of 951Mt of CO₂e emissions, largely due to shifting agriculture, forestry, and wildfires. (There is quite a lack of deforestation data in other sources, which makes it difficult to corroborate with semi-accurate trend-wise data.)

Afforestation in other wasteland and barren areas may seem like a win-win-win approach in increasing areas of carbon sequestration, but research from May 2021 showed that such planted trees do not always increase net carbon sequestration. They can end up contributing to greater occurrence of fire or reduced soil conditions, and non-native “tree invasions” can have negative effects on the local biodiversity, economic opportunities, and water yield.

There are green shoots

It is possible that the relative success of India’s two other Paris Agreements targets has led to less emphasis and direction on this 3rd target on forest-based carbon sinks.

Or it may be the more overt clash (than the other targets) it faces with India’s development and economic growth priorities that hampers concrete efforts.

But there are encouraging steps, in off-government activities even, that can show a path for some significant progress in the coming 9 years.

A lot hinges around preserving and maintaining existing forest land. Soil-based carbon credits are starting to grow in agricultural areas, as a way of opening up a significant store of economic value in maintaining plantation and tree cover. Scaling this to forest land is a tricky proposition, with issues in demonstrating additionality and providing an accurate measure of carbon stock. But there is potential for this to be an emergent space; soil could be a final frontier for carbon credits.

Private entities are stepping in to provide new ways and approaches to preserve forestlands. Rainmatter Foundation, an organization fast becoming a favourite of ours at CFI HQ, has committed USD 100 million to support individuals and organizations working on solutions around afforestation, ecological regeneration and livelihoods. This stands as one of the largest statements of intent for encouraging nature-based and nature-preserving solutions, including an entity focused on purchasing land to develop nature-based services.

Nature-based solutions on their own are also on the rise. We covered this in the last newsletter, with the largest philanthropic investment to the space pledged on the sidelines of the UN Global Summit in September. India has some history of practicing nature-based solutions, quite often linked to agriculture, but suffers from these not being implemented at scale, and with not much of a forestry focus.

There is also the hope that the COP26 summit can give a boost to government action. Calls for a new, improved Reduce Deforestation and Forest Degradation (REDD+) framework can create a better market for forestry credits that has been sorely lacking. Nature-Based Solutions is a core theme of the COP26 summit, amid a prominent call in UNEP’s State of Finance for Nature 2021 for up to USD 8 trillion to be invested into it by the mid-century. It could function as some impetus around which countries, like India, can place greater focus and resources on.

Time will tell how all these initiative translate into increase forest cover and carbon sinks. But time is also getting short. The developments over the next couple of weeks will give a look into the near-future priorities.

Engaging with CFI

As always, if you are keen to engage or talk to us on our work plans (check out the deck here) or if you have something of your own to collaborate on, reach out to us below!

That’s it for Edition #16 of our newsletter. Look out for the next one for our roundup of everything that happened at COP and what it means for the future of climate finance.

Also, we appreciate you sharing this with other climate finance enthusiasts.

Best,

Simmi Sareen and Shravan Shankar