CFI Newsletter #2: Less greenwashing; more green funding

+ the incubation-growth gap in climate startups, net-zero trends, reducing temperature rises, and getting to 100 Billion

The Climate Finance Initiative Newsletter offers quick digests and insights around what is happening in climate finance. While the Climate Finance Initiative’s current focus of work is India-centric, we will capture a global perspective of climate finance in this newsletter on a fortnightly basis.

The Climate Ambition Summit – the fifth year anniversary of the Paris agreement – that took place last weekend turned out to be a rather damp squib. India’s announcements, in particular, were not at all ambitious. It is tempting to drown our disappointment in mung bean salads (Boris Johnson said that’s what we eco-warriors eat; plus we, at CFI, rather like our moong dal). But read on, instead, to discover a few bright spots that emerged this fortnight in the world of climate finance.

Climate Finance by the Numbers

2.1 degrees Celsius

A 2 degrees increase from pre-Industrial age levels is what the Paris Agreement targets. 1.5 degrees is what is ideal. 2.1 degrees is highly promising.

127 countries, accounting for 63% of current global GHG emissions, have committed to net-zero emission targets either by 2050 or 2060. This includes Joe Biden’s election pledge for the USA to be at net-zero by 2050. If the other 37% follow suit, we can expect the temperature increase to drop further than the 0.1 degrees Celsius needed to be in with the Paris Agreement goals.

Absent from the 127, is India, the 4th largest emitter in the world. We covered India’s reticence towards more progressive targets in the last edition of the CFI newsletter. We did hope that Prime Minister Modi’s brief speaking slot at the Climate Ambition Summit would give some indication of renewed targets or indicate when India’s INDC may be published, but there was not much beyond highlighting that India would meet its not very ambitious 2030 targets.

Issuing net-zero emission targets are not enough. Countries need to revise their near-term 2030 targets to be more in-line with these broader ambitions, something that the EU has done, and China has to a lesser extent.

We will be keenly watching what the 2020 vintage of other countries’ INDCs have to offer.

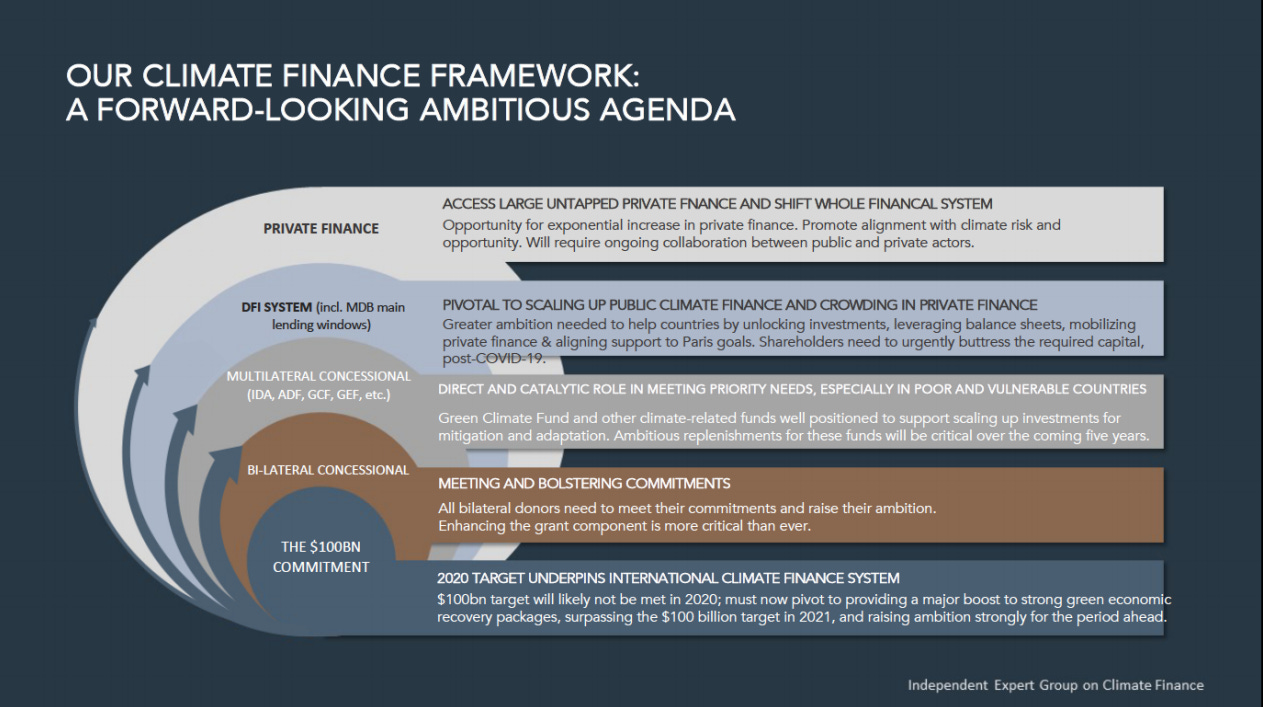

US$78.9 billion

In 2009, at the COP 15 Summit in Copenhagen the developed countries of the world pledged to mobilise US$100 billion a year by 2020 to help developing countries act against climate change. Fast forward 11 years, it is looking likely that this target will be met.

The IPCC estimates that US$3.5 trillion in investment by the mid-2100s, would be needed to reduce greenhouse gas emissions and keep warming below 1.5°C. We do have a long way to go, but this US$100 billion is important as it is the bedrock for catalysing the other forms of capital we need to scale climate finance to that figure.

Public finance plays a de-risking role in investments for transforming sectors and industries towards a low-emission, climate-resilient future. More financial instruments - from concessional loans, grants, to guarantees - to developing countries, create pathways that allow for larger bilateral, multilateral, development funding, and private financing to enter.

This is the aim in any case, and there is a long way to go. The US$100 billion may only amount to 2.86% of what we need, but it can help to unlock the capital we need towards the US$3.5 trillion that needs to be mobilised.

US$9 trillion

The combined assets of 30+ asset managers of the Net-Zero Asset Owner Alliance

The Net-Zero Asset Owner Alliance is a UN-backed group for asset managers to act on limiting global warming by running carbon-neutral investment portfolios by 2050 or sooner. This is climate action in finance that can have a real impact; financiers do not have a lot of carbon footprint themselves, but they do influence a significant amount of assets that get built and funded.

In the last few months, several large asset managers and banks have joined the Alliance, with Fidelity and UBS joining in the past week. Within a year of starting, the Alliance has mobilised 8% of the total assets under management globally to commit to this net-zero target, which is undoubtedly a positive trend that will only grow. And it starts with the sort of near-term targets we have been hoping to see in countries: the Alliance members will reduce greenhouse gas (GHG) emissions in their portfolios by 16% to 29% by 2025 from 2019.

Behind the numbers, however, there is a lot more detailing for these institutions to understand what constitutes the financed emissions in their portfolio. The growth of the Alliance should, however, create greater demand for number-crunching and data analytics. With that comes tools and solutions that will improve visibility, transparency, and trust in the numbers published from initiatives that tackle GHG emissions - something that can de-risk and open up more capital markets to climate action.

Less greenwashing; more green funding

Energy-efficient lights and fewer flights are not how financing institutions should tackle climate change

Large corporations often use carbon offset programs to then continue their carbon-emitting lifestyles. Paying for growing more forests or saving forests from getting cut down helps to even out their business’ negative impact on the climate.

Such carbon offsets are problematic. Their impacts are difficult to measure and quantify. Bloomberg recently reported on the multiple problems with the way The Nature Conservancy, one of the oldest and largest environmental groups, claims these climate offsets: one of which was carbon credits being claimed for saving forests that were never at risk in the first place. In the line of fire were millions of dollars paid by JP Morgan and Blackrock to preserve forestland.

Nature Conservancy has denied these reports and we do not know if we are dealing with fake carbon offsets here or whether it is a situation where real impact is incredibly hard to measure. What we do know is that funders - banks, private equity firms, asset managers - have an opportunity to create climate impact beyond carbon offsets.

Financiers may generate a tiny amount of emissions from their own operations but they control how trillions of dollars in capital is deployed in activities that lead to significant emission generation - financed emissions. Since the beginning of 2020, we have seen several large funders doing just that. Blackrock, Deutsche Bank, MUFG and many other banks and asset managers have commitments to stop funding coal-fired power plants. Twenty-five major insurance and reinsurance companies globally have stopped insuring coal projects.

Taking money away from coal is obviously no guarantee that those trillions of dollars will be deployed in green assets. But take the stock market as a corollary. All of the past year, even as COVID-19 impacted economies and businesses globally, stock markets around the world hit record highs. The markets are booming, not because of investor confidence in underlying stocks, but because other asset classes give even less returns and money has to go somewhere. Similarly, we hope that when funders cannot or will not fund coal, they will end up with excess energy sector allocations that will be deployed in climate-positive assets.

There are still holdouts of course. Warren Buffet continues to fund fossil fuels. And when Adani Group could not find funding for its Carmichael mining project from Australian banks, the State Bank of India stepped in for not very clear reasons; but this decision has started to face significant shareholder criticism.

As more funders and insurers make public commitments, it is getting harder to finance and insure fossil fuel projects. This is one change we hope will continue to drive significant positive movement in climate finance in the next few years.

The Incubation-Growth Gap in Climate Startups

Early-stage funding and innovation structures in India need an urgent rethink if we are to effectively support entrepreneurs to build solutions that address climate change

If you are a budding climate entrepreneur in India looking for an early-stage entrepreneurship program to validate your idea or prototyped solution, you are in luck.

You get the choice of boot camps, incubators, innovation challenges from academia and universities, companies, government, fund-linked platforms, diversity support platforms, foundations, think-tanks, multilateral organizations, and more.

After the program, you might have got your validation, and, if offered, you might have even got a small equity-free grant from 3.5 lakhs to 15 lakhs (~ US$5,000 to US$20,000).

Things get tougher when you start looking for further support to grow.

It is a pretty barren space unless you are in a position to do a US$10 million or so round from a tech-focused VC firm with a climate portfolio - who still do view climate as a high-risk space against other sectors, and seem to employ a survival of the fittest type of approach to backing startups. There are impact-focused funds like Menterra and the newer Rainmatter Climate cutting earlier cheques, but they are few and far between and concentrated in specific areas.

The gap exists.

And it is reducing the success of promising solutions to scale. It is also slowing the pace of adoption of climate-positive solutions, at a time we need to act with more urgency on climate change.

This area between idea validation and getting to the stage of being able to a US$20 million round, which we at CFI term as the Innovation Support Ecosystem, needs an urgent rethink.

It requires a relook on how promising technology should be validated, the financing and support structures needed to bridge the gap, and how further funding entities need to be engaged to reduce climate action’s high-risk tag.

Our report on The State of Climate Finance offered a quick glimpse into two on fixes and improved financing structures we felt would help:

A technical, demonstration fund that evaluates the innovations and funds them to an actual working product. If innovations have to fail, let them fail fast and fail often so focus can shift to other, better working solutions.

A business aggregator that assembles a team of finance, marketing, compliance and legal experts, and invests in converting technologically proven products to functioning business ideas, allowing the innovator to still lead but focus more on product and tech.

Our next report, with a planned publishing date of January 2021, will offer a deeper dive into this Innovation Support Ecosystem, a more quantitative diagnosis of today, and fleshing out we need to build to bridge the Incubation-Growth gap.

If you have any perspectives on what is happening in this space, reach out to us! We would love a conversation.

Engaging with CFI

We are looking to engage with the wider climate finance ecosystem and we invite you to reach out to us through the links here:

If you are a funder

If you are a finance professional

If you are a climate entrepreneur

If you have our emails, of course, do drop us a line. Apologies to those of you who have reached over the past couple weeks. The end of the year crunch has picked up and we will get back to you asap for a chat :).

Finishing School for Climate Data and Analytics Startups

A reminder that we are planning for a finishing school program in 2021 to support climate-focused number-crunching and data analytics solutions and companies to reach out and engage with financing and funding entities.

If you are keen to explore this, do reach out to us through the button below:

This is us signing off on the last newsletter of the year. Happy Holidays, and hope the next year turns out a lot less strange and a lot more green than this one.

As always, send all feedback, compliments and brickbats our way. And of course, we do appreciate you spreading the word about this newsletter.

Best,

Simmi Sareen and Shravan Shankar