Climake Newsletter #23: Plastic's EPR Innovation Drive

+ the economic impact of biodiversity loss, a big funding push for EVs, the phenomenon of increased rainfall, and diwali crackers

The Climake Newsletter offers quick digests and insights around what is happening in climate finance. While Climake’s current focus of work is India-centric, we will capture a global perspective of climate finance in this newsletter on a fortnightly basis.

Diwali is coming up and that means it is time for the annual tradition around air pollution and firecrackers. Despite the scrutiny, and the obvious excess smoke that can reduce visibility to about 10 feet, the contribution of bursting crackers on India’s air quality is hotly debated. There is clear evidence that air quality levels drop the day after Diwali, but research earlier this year pointed the issue more towards biomass burning rather than crackers and that cracker bans in Delhi had little effect on air quality. This debate has had an impact: with the rise of green crackers and a growing number of households not looking to burst crackers.

Regardless of how you wish to celebrate it, we, at Climake HQ, wish you and your family a very Happy Diwali

Climate Finance by the Numbers

USD 1.9 trillion

The potential economic loss at stake arising from biodiversity and nature-related risks

Biodiversity losses, due to increased climate change and other effects, have often been linked to the impact on the natural environment, such as the roughly one million animal and plant species that are at risk of extinction. But its financialization and the impact to business can offer some more urgency to act.

Moody’s identifies 9 sectors that affect or depend heavily on natural resources - land, air, and water: metals and coal mining, oil and gas, building materials, environmental services and waste management, steel, livestock and agriculture.

The cost of USD 1.9 trillion comes the exposure of these sectors predominantly from two main types of biodiversity risks:

extractive industries, such as coal mining and oil and gas exploration, that damage natural ecosystems that reduce their ability to extract more

sectors dependent on ecosystem services of natural resources that getting depleted and degraded affect make sectors such as agriculture, fishing, and even tourism vulnerable

The impact of inaction on biodiversity loss and the need to preserve natural assets and resources, can be greater. About USD 44 trillion, roughly half of the world’s GDP, depends on the natural ecosystems in some way.

Investments into preserving or improving biodiversity and nature-based interventions have been largely dependent on grants and similar non-risk based capital, which has been too small to mobilize for the gravity of the problem.

But we have started to see some urgency and change. Biodiversity investments are estimated to reach as much as USD 93 billion by 2030, up from USD 4 billion in 2019. There is also the rise of hyper-focused venture funds focused on addressing targeted areas of biodiversity loss, such as Convective Capital that has raised USD 35 million purely to back technology that only tackles wildfires - an increasingly significant area of biodiversity and economic loss, but whose importance can be put into greater perspective by the SwissRe estimate that 70% of all economic losses from wildfires have been claimed in the last 5 years.

USD 1 billion

77% of all vehicles in India are financed through loans, with the commercial vehicle, 2-wheeler and 3-wheeler segments most reliant on credit financing. These are the same categories that are driving India’s EV sales. Scaling credit financing is an important factor for the growth of this sector.

There are primarily 3 types of EV lenders: banks, NBFCs, and leasers; sector-focused NBFCs and leasing companies have been at the forefront, taking higher risks in supporting financing to EV companies, that often, especially in the 3 high-growth segments, are newer ventures and enterprises than traditional automotive OEMs. This nascence makes lending to EVs higher risk, as well as the willingness of buyers, especially B2B buyers to purchase from EVs.

The proposed USD 1 billion loan guarantee fund offers to be a game changer in improving confidence to buyers and encourage lenders to issue loans. A loan guarantee works by a third-party between the lender and the EV company, the guarantor, offering to cover a portion of any loans that may default - thereby allowing the lender to mitigate losses and incentivize offering loans.

We are keeping a keen eye on how the fund influences the growth of the sector-focused NBFCs and leasing companies, especially as the guarantee funds should incentivize more risk-averse banks to get more into EV lending. The number of EV financing startup plays have increased from 4 to 13 over the past year, and led by the likes of Grip Invest, RevFin, and Three Wheels United, have been attracting increased sums of venture capital to leverage an expected tech-enabled and domain-focused approach for improved lending. How will this shape up?

The World Bank-SIDBI loan guarantee fund is a sign of bullishness that the EV market in India is going to go big. EV sales, by vehicles sold, grew for the first 9 months of the year grew by over 70% as compared to the same time period in 2021. The 2022 sales, up to September, amounted to 656,098 EVs sold, about 4.6% of total vehicle sales in India. In 2021, this share was just 1.8% of all vehicles sold. The trend of India’s EV market is up.

10,000%

September is the kharif harvesting season in Uttar Pradesh, where crops grown on the back of the summer monsoon should be ready and ripe for plucking. The issue is not just increased rainfall, but its erratic patterns. The 10,000% increase in rainfall comes on the back of droughts faced by this same region, where rainfall was below average in 96% of districts in the state. This increased rainfall intensity, more associated with monsoon conditions, has occurred when the summer monsoon has been in retreat.

A warmer world due to climate change effects will lead to a wetter world, with more rainfall intensity and flooding expected. We are seeing the incidences of this with more frequency and damage, from Pakistan, to China, to Latin America, it is increasing globally.

Extreme rainfall leads to a USD 3 billion worth of loss and damage every year in India. The loss and damage is experienced largely through extreme flooding which affects urban and rural infrastructure and property, agriculture produce, transportation lines, and also leads to loss of life.

These effects will only increase in a warming world. We need a more urgent focus on adapting and mitigating such effects, through climate adaptation solutions. For agriculture, these can can range from on-farm water management, soil resilience approaches, to nature-based drainage solutions. As we have covered before, here and here, climate adaptation has not picked up to the level that we need; in terms of policy targets, investment, and most importantly, private sector involvement.

Most climate targets of countries focus on mitigation around achieving net-zero. Such a large-scale policy signalling has a knock-on effect from the private sector of industry and capital providers to focus on supporting climate mitigation solutions. Adaptation struggles to mobilize resources and capital to a similar level, due to a lack of a similar big-ticket lightning rod of policy to attract private sector involvement - something that is urgently needed.

This is despite India having a National Adaptation Fund for Climate Change, that has mobilized almost USD 100 million for projects across India over last 7 years, largely from other government funding sources, and barely anything from the private sector. While this number may look significant, it pales in comparison to the expected low billions we will need to invest annually for climate adaptation.

THE BIG READ

Innovations of India’s Plastic EPR

Plastic Extended Producer Responsibility (EPR) norms in India have the potential to transform plastic waste into a useful commodity by incentivizing different areas across the packaging value chain. We forecast what sort of innovations India’s Plastic EPR norms will drive.

In our last Big Read, a guest post by Anthony Randazzo of the US International Development Finance Corporation, offered a compelling case for how India’s Plastic Extended Producer Responsibility (EPR) norms has the potential to be a driver for innovation and impact.

It got us, at Climake HQ, thinking as to what types of innovations would benefit or be driven from these norms. What would be new or upcoming areas of innovation that will be incentivized and present as opportunity areas for growth. This is what we explore today.

Plastic EPR’s Innovation Drive

So what sort of plastic circularity solutions is EPR expected to incentivize?

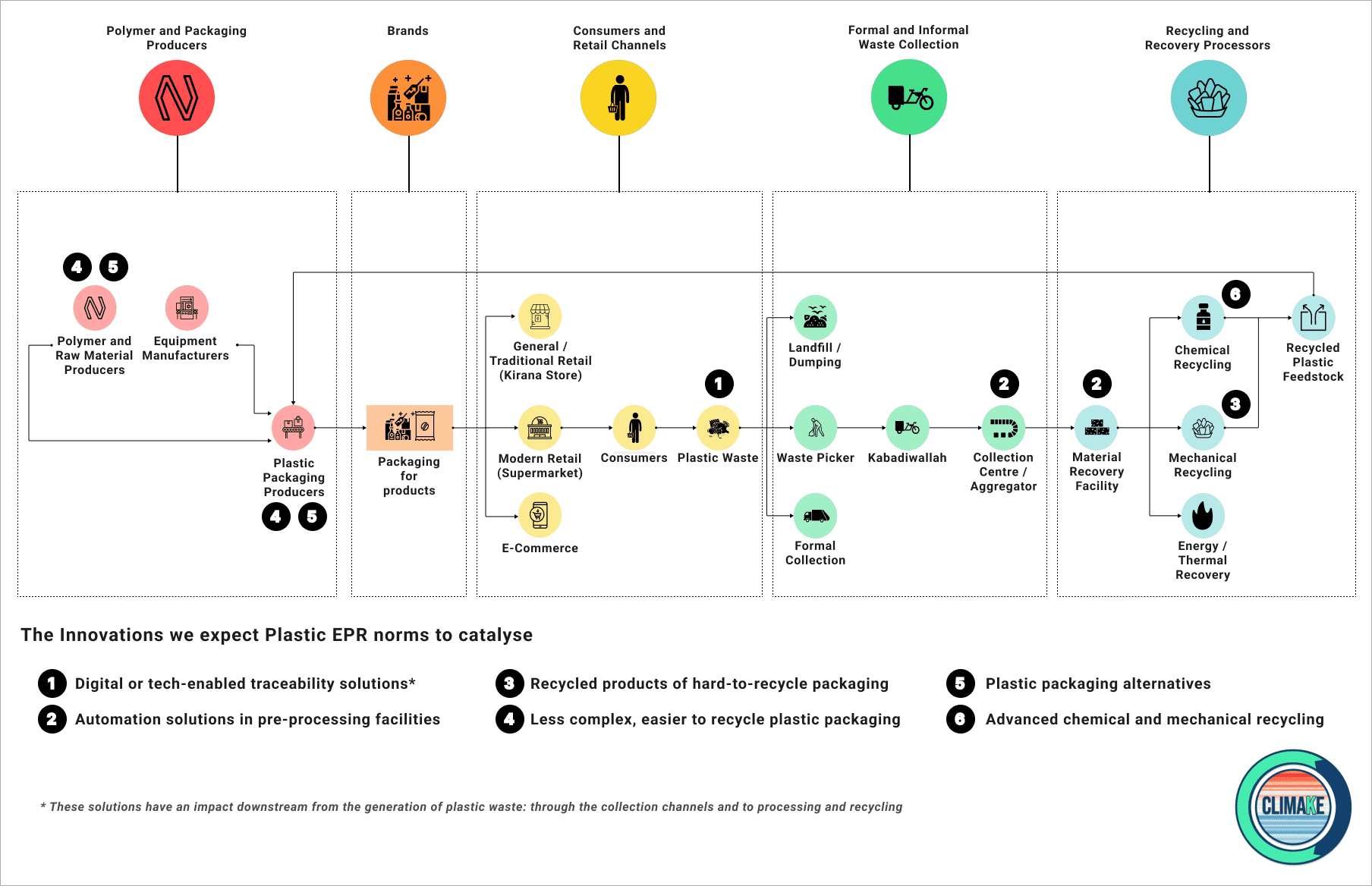

Here’s a simplified outline of what the plastics packaging value chain looks like, from production of plastic packaging to how its wastes are managed.

+(1).png){kind=link}

We expect 6 types of innovations to directly benefit and be catalysed as a result of the Plastic EPR Guidelines (the numbers listed 1 to 6 in the image above, that also show where we expect these innovations to be adopted)

One area that we recognize, but do not cover here, are ones at the informal sector of waste pickers and kabadiwallahs. This informal sector collects up to 50% to 80% of the recyclable plastics in India. An increase in expected volumes should see a knock-on effect to the informal sectors in the form of improved livelihood opportunities, support, and working conditions to strengthen this collection backbone of the plastic recycling value chain. We expect this to come from solutions and steps that improve access to services, to formalization and its benefits, and similar approaches that rely on on-ground engagements with the informal sector.

In this Big Read, we have opted to focus on technology innovations. Here is our 6 areas, and how and why they will the Plastic EPR norms will make them grow.

1. Digital or tech-enabled traceability solutions

These solutions have benefited from the documentation and traceability expectations for EPR compliance, across the waste value chain, that has been around since the first version of the EPR guidelines. To be more effective, traceability tech needs to be integrated with on-ground activities, such as through trackers with digitised weighing machines. It helps to ensure a better quality of plastic wastes transferred and reduce the risk of double-counting, which are prevalent issues, especially through smaller 3rd party waste facilities, where currently manual entry can be the main approach.

Recykal, founded in 2016, is a leader in this space, having collected over 200,000 metric tonnes last year through its B2B traceability-driven marketplace. Their latest raise of USD 22 million, in January 2022, is reflective of the need to integrate digital technology with on-ground operations. A significant share of their raise is devoted to building their own hyperlocal waste management infrastructure to integrate software with on-ground operations.

2. Automation solutions in pre-processing facilities

Automation in pre-processing facilities (specialising in initial collection to material recovery) has also increased in adoption. Such facilities sort and pack plastic wastes into desired grades and types before being sent to a recycler has increased in adoption. Automated segregation, in particular, which leverages optical imaging and machine learning, has started to get adopted in large-scale facilities, such as MRFs. NEPRA, one of India’s largest waste management players, has deployed such equipment at its large-scale MRFs in Indore and Ahmedabad. As a sign of the company’s bullishness on automation, they have set up a linked entity focused entirely around automation solutions for plastic wastes, Ishitva Robotic Systems.

However, automation in smaller facilities has been limited even with developed and trailed solutions such as Vinglabs. This may be due to costs and minimal efficiency gains, as scalability and commercialization within this domain still remain undefined. The need for digitisation is arguably more in smaller facilities which are closer to the source of plastic waste generation; there are more chances of mixing and contamination at this point making sorting more complex later on.

3. Recycled products of hard-to-recycle materials, e.g. multi-layer plastic (MLP)

Brand owners will have to recycle 30% of their MLP packaging targets from 2024, a number that will progressively increase to 60% by 2028. Unlike more recyclable rigid plastics, MLP has seen little recycling potential. There have been moves to use it as a building material in panels (see Ricron Panels and Plastics for Change), but most MLP waste goes to thermal recovery activities. The state of recycling approaches for MLP is so nascent that it can be said to be in the R&D stage. Given the popularity of MLP packaging, however, we do need to look for recycling solutions fast.

4. Less complex, easier to recycle plastic packaging

Less complex relates to moving to packaging formats that are easier to recycle and handle after use. For MLP this is moving away from the “multi” part; packaging materials made from one layer or type of plastic, such as high-density polyethylene (HDPE) are easier to recycle than a mix of plastic, paper, and aluminium. This is not an easy proposition as MLP offers barrier protection and flexibility benefits over most types of packaging, and transitions to “mono-layer” have been limited. However there has been progress, with the likes of Huhtämaki, one of the largest packaging producers globally, developing a new range of recyclable flexible packaging which can replace MLP with a single layer laminate in the poster child for plastic waste: small shampoo sachets.

5. Plastic packaging alternatives

We do need to talk about plastic packaging alternatives such as biodegradable natural materials and reuse and refill solutions, even as we expected EPR to be a limited driver for their adoption. These alternatives require significant changes to how products have to be designed and sold to consumers. Mainstream EPR targets enable brand owners to have limited changes to a product’s packaging.

Solutions like ZeroCircle and Refillable, however, have had some traction in providing alternatives, and while certain brands may see the benefit of reducing their EPR targets by adopting these alternatives, we feel their adoption will come more from other drivers, such as voluntary company commitments and meeting consumer demand.

6. Advanced chemical and mechanical recycling

By 2028, over 60% of plastics packaging will have to be recycled, including currently hard-to-recycle plastics, such as multilayer plastics. Recycled content in packaging will also become mandatory in increasing numbers. Chemical recycling allows plastic wastes to be broken down into building blocks as second raw materials to be remade into new products, a similar, but more comprehensive, process to making plastic fuel through pyrolysis. Chemical recycling has not been widespread due to the significant costs and lack of demand, but companies like PolyCycl that have had extensive research in this, are poised to take advantage of the have been making steps towards this, and future demand, and more secured supply, should see chemical recycling becoming commercially viable in the coming years.

Organizations like Banyan Nation have been at the forefront of making recycled plastics from rigid plastics, through mechanical recycling, more mainstream. A future opportunity here is in food-grade plastics. Food and beverage, personal care, cosmetics, and pharmaceuticals are all large users of plastic packaging that needs to be food-grade. An upcoming policy around recycled plastics use in food-safe applications is reflective of the need for more innovation to create food-grade recycled plastics, but this is a u-turn from a December 2018 statement from the Food Safety and Standards Authority of India, claiming that recycled plastics should not be usable in food-grade plastics.

EPR-led innovation is an opportunity area

The latest EPR Guidelines have faced questions of being feasible in meeting these ambitious recycling targets while the infrastructure and innovations to meet them are not currently present. But it is the sort of objectives that are needed to tackle India’s plastic waste issue, and it does present an opportunity for innovation in these areas. After all, as we have experienced many times, nothing drives adoption of new solutions and innovation as effectively as compliance mandates, and a highly visible regulation like EPR should see a lot of growth for that.

The norms create the sort of incentives, from market size, nascence of solutions, and urgency for solutions to be adopted, to make plastic circularity, a high-impact sector to attract research and investment.

Plastic recycling rates for India varies from 30% to 50% and even 60% of plastic waste generated, the differences due to how recycling is defined. If we take the strictest, and most needed definition of recycling - where plastic wastes are made into second-life raw materials that could be used to make new products - this rate would be at the lower end of the range. By 2028, India targets to have between 60% to 80% of all plastic wastes to be recycled; plastic wastes generated in 2028 are expected to grow by almost 50% from today’s numbers. This is the sort of need and opportunity for these innovations we outline to be scale.

We estimate that around USD 50 million of venture equity was invested into plastic circularity innovations in 2020 and 2021. EPR’s push towards recycling should provide incentive enough for startups and investors for this number to increase exponentially.

That’s it for Edition #23 of our newsletter.

As always, send all feedback, compliments and brickbats our way. And of course, we do appreciate you spreading the word about this newsletter.

We’re growing to build things collaboratively and the more the merrier!

Best,

Simmi Sareen and Shravan Shankar