Climake Newsletter #31: Tackling Methane Emissions in India

+ financing for a 1.5°C pathway, emission gaps and global temperature increases, and blended finance's emerging role in climate finance

The Climake Newsletter offers quick digests and insights around what is happening in climate finance. While Climake’s current focus of work is India-centric, we capture a global perspective of climate finance in this newsletter on a monthly basis.

The Climake newsletter is back. We have been on hiatus for a while; but now that we are past the thick of the conference season and the COP, it seems like the right time to start exploring new themes in climate finance. COP29 in particular, provided a guidepost to us finance enthusiasts in the form of the new USD 300 billion funding commitment from developed nations. The exact details of how this USD 300 billion will flow to developing nations are yet to emerge, and many believe it is still way too little an amount, it is at the very least a step up. We will keep following the space to figure how and where this funding flows, and if it progresses (as promised) to an expected USD 1.35 trillion a year by 2035.

There has been much else to keep us busy in the meantime. From the plethora of reports that came up over the last few months, we have picked our top 3 below to give you some insights on what the climate finance world is focusing on beyond COP, and for our big read, we cover how India needs to tackle methane emissions.

Climate Finance by the Numbers

USD 7.46 Trillion

Climate Policy Initiative’s latest “Global Landscape of Climate Finance 2024” reported that annual climate finance flows doubled from between 2018 and 2022, from USD 674 billion to USD 1.46 trillion. Climate finance flows in 2023 has also likely exceeded USD 1.5 trillion, led largely by investments in renewable energy and low carbon transport. Mitigation finance continues to dominate climate funding overall, accounting for USD 1.3 trillion or ~90% of all climate finance flows in 2022.

Private finance accounted for 54% of mitigation flows in 2022, with strong growth in the buildings and infrastructure sector as well as transport, indicating that such projects are becoming more commercially viable for private capital. However, investments outside climate’s three key sectors (energy, transport and building infrastructure) have remained low.

Adaptation finance doubled from 2018 to reach USD 76 billion in 2022. This, however, is insignificant compared to the mitigation investments, and way below the need for adaptation investments today. The sector continues to be viewed as ‘public goods’ with public sector providing the bulk of the adaptation flows (92% in 2022).

Between 2018 and 2022, a large proportion (44%) of adaptation finance went to the water and wastewater sector, which aims to reduce water stress induced by climate change via both water supply and wastewater treatment projects. Cross-sectoral projects—including policy support, capacity building, and disaster-risk management—also featured heavily in the adaptation landscape (36%). However, the report estimates that adaptation investments remain way below even the most conservative estimates of around USD 212 billion needed till 2030 annually.

A significant uptick is needed in both mitigation and adaptation funding. Although climate finance flows doubled between 2018 and 2022, a further fivefold increase is required annually to keep global warming below 1.5°C. The need to raise this USD 7.46 trillion in funding a year is also time critical. The projected economic losses that can be avoided by 2100 by realizing a 1.5°C warming scenario are estimated to be 5x greater than the climate finance needed by 2050 to achieve it.

What surprised us: We certainly hadn’t realised that China is 42% of all climate finance globally. That’s more than all developed nations, combined!

3.1 degree Celcius

UNEP’s annual Emissions Gap Report offers a yearly tracking of our progress towards limiting global warming. The 2024 report highlights that based on current global policies we are likely to overshoot these limits, reaching 3.1°C by 2100, with annual global GHG emissions projected to be 57 GtCO2e in 2030. If we are to limit warming to 2°C, annual emissions will need to reduce by about 5.5%; while a 1.5°C pathway will require emissions reducing by 9% every year until 2030. Global GHG emissions in 2023 reached a new high of 57.1 GtCO2e: overshooting the projected target 7 years in advance, is not an encouraging trend.

More needs to be done is common knowledge to almost everyone.

The report gets to outlining what is needed, with the figure above outlining the mitigation potential across different sectors. And, yes, as expected a key, yet unsurprising finding is that we already have available, cost-competitive solutions that can make a significant dent in reducing the emissions gap; policies and national plans do not have clear decarbonization pathways to make this happen.

Take, energy transition, for example. Increased solar and wind power adoption for energy generation, alone has the potential to reduce a third of our total GHG emissions. A more comprehensive energy transition may require us to focus beyond just building renewable capacity, to increasing demand side efficiency measures — such as grid efficiency and connectivity, and electrification and fuel switching in the buildings, transport and industry sectors — but solutions even for these are present, and not lacking.

The maximum temperature identified in the 2023 version of the Emission Gap Report was 2.9°C, putting a spotlight on the rate of increase of global temperature pathways and the need for more drastic steps. But we are operating in a scenario where climate action solutions in high impact areas like energy, transport, and forests hold real promise for sweeping and fast emissions cuts. Policies still lag behind what is needed, and a prolonged delays may only see that expected temperature incrementally increasing.

USD 18.3 Billion

The total blended finance flows towards climate investments in 2023

Blended finance has been spoken as a key component to unlock the billions and trillions needed for mainstreaming climate action (we have spoken about it before). It is an expectation that is starting to be realised.

Climate-focused blended finance accounted for USD 18.3 billion in 2023, and is today the largest focus of blended finance globally. Convergence’s State of Blended Finance 2024 report reflects an instrument that is maturing in importance. The share of climate deals sized at USD 100 million or greater was 56% in 2023, up from 23% in 2022, while the average ticket size of a deal grew over 160% in 2023 to USD 105 million. There were 6 blended finance climate transactions sized USD 1 billion or greater last year.

However, this growth has primarily been driven by mitigation finance, where technologies and companies are more mature and market-ready. Mitigation attracted 57% of all climate blended finance (five of the six USD +1 billion blended finance deals were for utility-scale renewable energy projects), while cross-cutting deals that are often mitigation first, but also provide adaptation, accounted for 36%.

Pure-play adaptation only accounted for USD 1.2 billion of funding, a 400% increase from 2022, but almost all from public finance and multilateral development banks. Private sector investments surged from USD 6.2 billion in 2023 from USD 1.8 billion in 2022, but the emphasis has been on mitigation, while DFI capital which often comes with concessionality saw the same trend.

Blended finance might have a risk averseness to bring capital to more hard-to-finance sectors (that arguably have a greater need of derisking to attract mainstream capital), but the main thesis that blended finance is maturing stands true. This is best shown by the trends of the type of “blends” that are being leveraged.

Concessional guarantees and risk insurance grew by almost 180%, while the use of technical assistance has been declining: blended finance’s focus is more towards tailoring finance instruments to be relevant to the existing nature of enterprises and projects, instead of the traditional norm of providing grants and technical assistance (TA) in the hope of getting projects and enterprises to a level that might be relevant for existing commercial instruments, with limited guarantees.

With emerging markets borrowing at rates nearly five times higher than developed markets, and estimates that nearly 50 emerging market economies would default if they invested what was necessary under their Nationally Determined Contributions (NDCs) over the next five years, the need for blended finance as a critical component of the world’s climate finance stack is clear.

THE BIG READ

Tackling Methane Emissions in India

A deeper look into methane abatement technologies and financing needs

The discourse on climate action often considers all emissions as the same. Greenhouse gases (GHG) emissions are counted as one big target number to be reduced. But all emissions are not created equal.

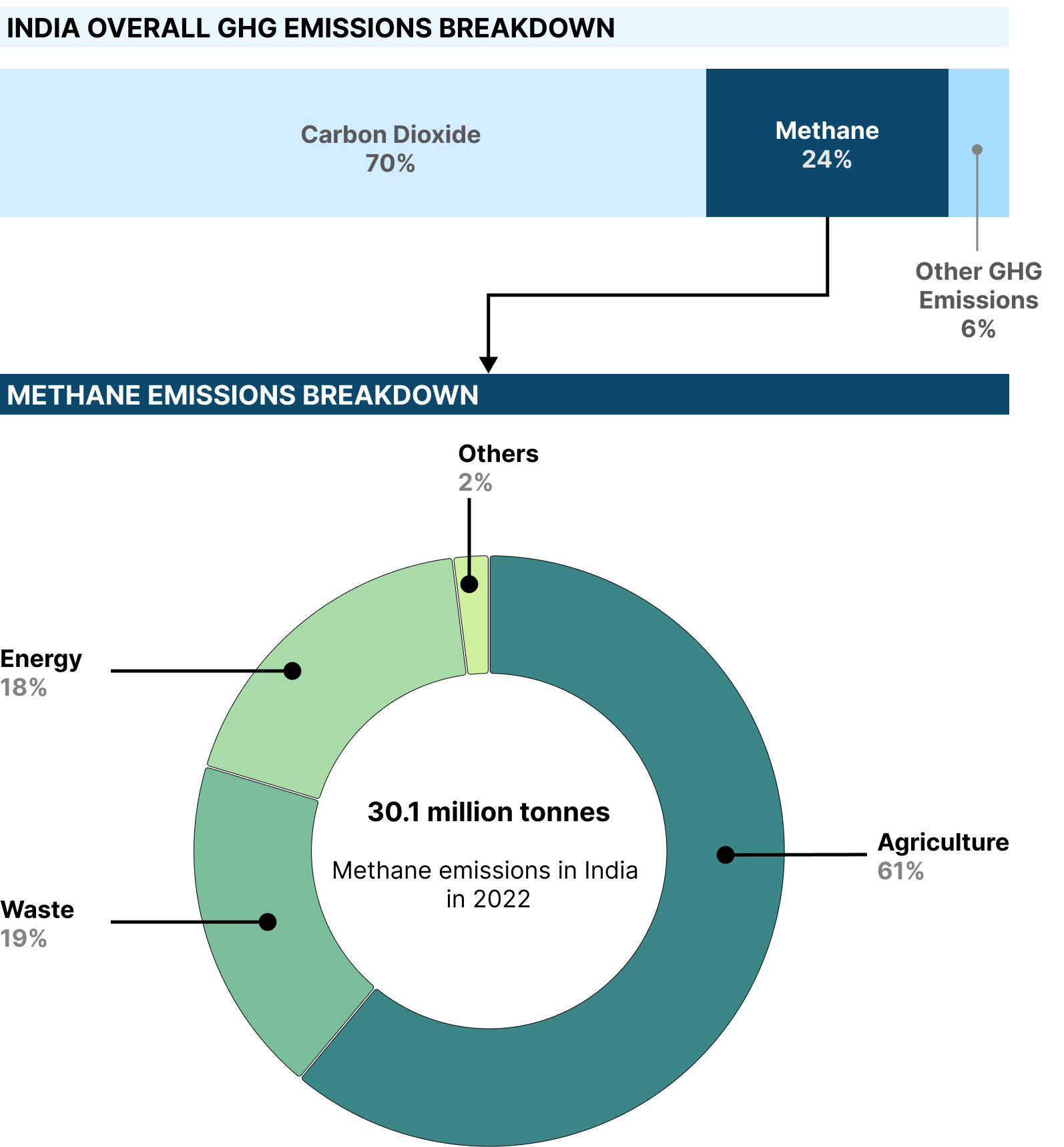

Methane is a greenhouse gas 2.75 times lighter than carbon dioxide but with a much larger impact on near-term warming, with a 20-year warming potential more than 80x that of CO2. Atmospheric methane concentration is rising constantly, and is now at 2.5 times the levels compared to pre-industrial era, and is responsible for 30% of our climate-change induced global temperature rise. Besides being a significant contributor to climate change, methane emissions also lead to generation of ground level ozone, a dangerous pollutant that affects air quality. An immediate and rapid reduction in methane emissions is necessary for any pathway that keeps global warming below 1.5 degrees.

Methane emissions have grown marginally since 2019, but curtailing its emissions is significant. Methane lasts in the atmosphere for only 10 years, unlike the hundreds of years that carbon emissions are present for: If we were to remove methane emissions today, we would eliminate its effects in the atmosphere as well by 2034.

The Global Methane Pledge, was introduced in 2021 to get countries together to create global action on reducing methane emissions, with a reduction of 30% from 2020 levels by 2030. The Pledge has 159 signatories, with nearly a 100 of these countries also devising national methane plans.

India is not a signatory to the Global Methane Pledge, nor has it formulated a national methane plan. Tackling methane emissions has not been a core priority for the country’s net-zero ambition. It is not feasible to even determine what India’s methane action finance need or gap is. But with the impact methane removal can have in reducing emissions, it needs to become a focus area for India, from driving sector level policy changes, and to enabling private sector innovation, and attracting finance.

Where Are Methane Emissions Coming From

Annual global methane emissions are around 580 million tons, with human activity accounting for about 60% (345 million tons) of emissions every year. India accounts for 30 million tons of these emissions, the composition of which differs from rest of the world: agriculture sources accounts for more than 60% of India’s methane emissions, while globally its contribution is around 40%.

Agriculture emissions mainly come from two sources: enteric fermentation and paddy cultivation. Waste sector emissions mostly originate from landfills as organic matter breaks down over time. The energy sector emissions come from a variety of sources. Coal contributes 55% of energy-related methane emissions, while bioenergy accounts for about 25%. Methane emissions are often depicted by the image of an oil refinery flaring waste gases — fossil fuel-linked emissions account for about 25% of overall methane emissions — however oil and natural gas contributes to only 4% of India’s methane emissions.

India’s focus on methane technologies and financing will be divergent from the rest of the world. Fossil fuel emission reductions have been the focus of most methane reduction conversations and funding commitments globally. India’s focus would instead be mainly on emissions from agriculture, waste and coal.

Technologies for Methane Abatement Exist; Scale Remains A Challenge

Agriculture-Related Methane Emissions

Agriculture sector emissions in India primarily stem from two sources: ruminant animals (principally cows, buffalos and sheep) and rice production. Ruminants create methane during digestion, along with CO₂ and other gases. Ruminants account for almost 70% of agricultural emissions globally and are responsible globally for more carbon dioxide equivalent (CO₂e) emissions than every country except China. These are emissions that can be partly addressed by a combination of reduce cattle use (for example, via meat and dairy alternatives). Technologies for addressing ruminant emissions at source also exist, primarily in the form of feed additives that reduce or eliminate methane emissions.

The second major source of methane emissions — rice cultivation — can also be addressed with existing technologies. Rice farmers would need to change long-established farming practices, including adopting new fertilization and water-management techniques, planting seeds directly in dry soil instead of transplanting young crops into flooded fields, and using aerobic rice varieties that can be grown without flooding and are more tolerant to droughts.

The key challenge here is not technology: it is distribution. Methane abatement interventions will require farmers to adopt practices that typically cost more than their current solutions. For example, the feed additives required for cattle or the bio-stimulants that reduce paddy emissions cost more than traditional feed; a co-benefit (like higher milk or crop yield) is necessary for farmers to adopt such solutions at scale.

Waste Sector Emissions

The majority of waste sector emissions originate from landfills. This is one area where India has put in significant effort and is making progress via:

Diverting fresh waste away from landfills: India generates around 60 million tonnes of municipal solid waste (MSW) annually; of these about 50% is now being processing instead of going to landfills. Most large cities have made investments in collection and processing solutions, largely via tie-ups with private players who set up material recovery facilities that ensure that less waste ends up in landfills;

BioCNG: India’s Satat scheme, designed to promote BioCNG usage has dual benefit for methane emissions: these plants can take in organic waste that reduces landfill methane emissions. Additionally, agriculture residue is increasingly being sought as input material for bioCNG plants leading to lower emissions in the agriculture value chains.

However, bio-energy generation processes can create new emissions across its value chain and more technology interventions are needed to create processes that reduce methane emissions further. A move towards higher end biofuels that use an emissions neutral process will further reduce waste linked emissions, but most technologies in the space and nascent and yet to scale.

Coal-related emissions

Underground mining accounts for more than 85% of coal’s methane emissions. Methane is released primarily from ventilation, post-mining activities, degasification, and fugitive emissions from abandoned but vented mines. Coal-linked emissions abatement has received the least attention across all methane segments. This is one sector where emissions could also increase drastically if no measures are taken as coal mining capacities in India increase over the next decade. The IEA estimates that 35% of India’s coal-linked emissions can be addressed with existing technologies, with 12% abatement possible at no additional net cost over the technology’s lifetime.

We expect that in all cases but specially coal, the drive for adopting abatement technologies will need a combination of policy and corporate action. While government policy can kickstart such adoption, a push from say, net-zero steel demand, could catalyse a move towards emissions reduction in coal.

Financing India’s Methane Abatement

Two types of funding has remained the focus of methane discussions. Grants are necessary to drive innovation in technology to combat methane emissions across energy, waste and agriculture, as well as to build better data collection and monitoring systems. At COP29, grants totalling USD 2 billion were announced across all of these use cases for methane abatement.

The other financing need is for project finance to deploy and scale the technologies that lead to better methane emission outcomes. While data on methane project finance is harder to track, global funding for methane abatement was only USD 14 billion in 2022, with most of this financing deployed towards agriculture, land use and waste. South Asia accounted for only 1.2% of this overall number.

We believe while these low numbers represent lack of financing activity in methane abatement, part of it is also due to underreporting of methane investments. Because methane abatement solutions can come in variety of forms, specially in agriculture, identification of methane linked investments remains a challenge.

We looked through the investment data for India from 2020 to identify any businesses that have a methane positive impact throughout the agriculture, energy and waste value chains. The numbers are shockingly low.

Scaling methane abatement might need solutions that are different from the traditional equity and debt funding models. We believe a threefold financing intervention model is needed:

Increase grant funding and risk capital in the form of seed equity and capital flows that fund ‘first-of-a-kind’ technologies to support research and innovation in methane abatement technologies;

Funding of startups that are scaling and distributing these technologies; many in the waste space would require upfront capital expenditure to be funded for setting up waste sorting and bioenergy systems but these technologies are inherently profitable and can pay back over time;

Funding working capital and adoption cost for users: Specially in the case of agricultural emissions, farmers would need support to pay for the additional cost of adopting new technologies. Many, like new methods for rice cultivation, could provide increased yields or cost savings over time but early adopters will need incentives in the form of financing or grants/subsidies to pay additional costs for what is essentially an untested technology at this point.

There is also a case to be made for carbon markets to step in. For both agriculture and waste sectors, a permanent shift to sustainable, low emissions practices can be funded through carbon projects. Again, these markets have been in flux for the last couple of years and global policy shift will be needed to kickstart activity.

Methane abatement and financing needs more than one intervention. Most initiatives are at very early stage at this point but viable pathways exist to scale abatement efforts. Most would need a combined push from the Indian government, corporations and consumers to create the impact needed. The good news though, is that there are multiple technologies and startups working towards this change and many have sustainable, long term viability if we can solve for early capital gaps.

That’s it for Edition #31 of our newsletter.

As always, send all feedback, compliments and brickbats our way. And of course, we do appreciate you spreading the word about this newsletter.

Happy Holidays, and we will see you in the new year!

Best,

Simmi Sareen and Shravan Shankar